- Categories :

- More

How Your Home Equity Can Help the Next Generation Buy a Home in The Woodlands

By:

![]() The McClung Group

| Published 03/02/2026

The McClung Group

| Published 03/02/2026

Written by Jaubrey Amboy

Can your home equity help your child or grandchild finally buy a home?

Yes. If you’ve owned your home for years, there’s a strong chance you’ve built significant equity—and even a portion of that equity could help the next generation overcome the biggest obstacle to homeownership: the down payment.

The Equity Advantage You May Not Be Thinking About

If you’ve owned your home for a decade or longer, two powerful forces have likely been working in your favor:

- Home values have increased

- Your mortgage balance has decreased

That gap between what your home is worth and what you owe is your equity.

For many homeowners in The Woodlands, that number is substantial. And while you may view it primarily as a retirement asset, it can also serve another purpose—creating opportunity for your family.

At The McClung Group, we regularly speak with parents and grandparents who want to help but aren’t sure how it would work financially. The truth is, you may not need to use all of your equity. Even a strategic portion could make a measurable difference.

If you’re unsure what your equity position looks like today, that’s where a quick conversation helps. You can schedule a call with us to review your numbers and explore realistic options.

The #1 Thing Holding Younger Buyers Back

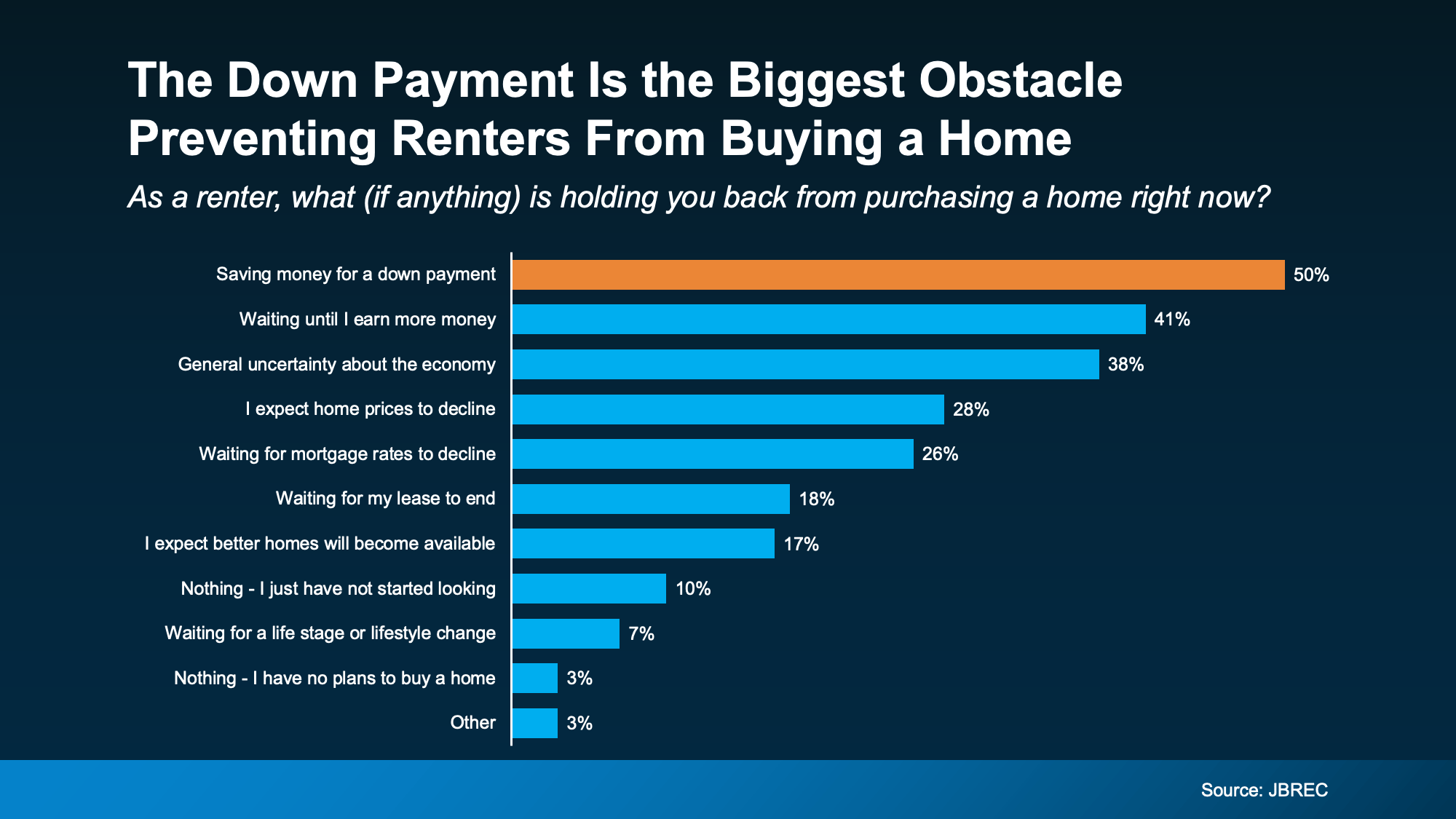

There’s a common assumption that high mortgage rates or home prices are the biggest barriers to buying. But research tells a different story.

According to John Burns Research & Consulting (JBREC), when renters were asked what’s holding them back from buying a home, the top answer was:

Saving money for a down payment (50%)

Other responses included:

- Waiting until I earn more money (41%)

- General uncertainty about the economy (38%)

- Expect home prices to decline (28%)

- Waiting for mortgage rates to decline (26%)

Rates and prices matter—but the upfront cash required is the primary obstacle.

Here is the data referenced:

That 50% number is significant. It tells you something important: if you remove or reduce the down payment hurdle, you remove the biggest barrier.

And that’s where your equity can change everything.

How Equity Can Be Used Strategically

There are several ways homeowners choose to leverage equity to help family:

- A cash gift for a down payment

- A structured loan to a child or grandchild

- Early inheritance planning

- Co-investing in the purchase

This doesn’t mean compromising your retirement. It means planning carefully.

With an estimated $68–$84 trillion expected to transfer from older generations to younger ones over the next two decades, many families are rethinking when and how that transfer happens. Instead of passing wealth down later, some are choosing to create opportunity now—when it can change a life trajectory.

The key is strategy, not impulse.

Before making any move, it’s wise to:

- Understand your current home value

- Review your mortgage balance

- Talk with a financial advisor or CPA

- Explore lending guidelines around gift funds

As Realtors in The Woodlands, we can guide you through how gifted funds or family loans are typically structured in real estate transactions.

If you’d like to see how this could work in your specific situation, schedule a call and we’ll map it out step-by-step.

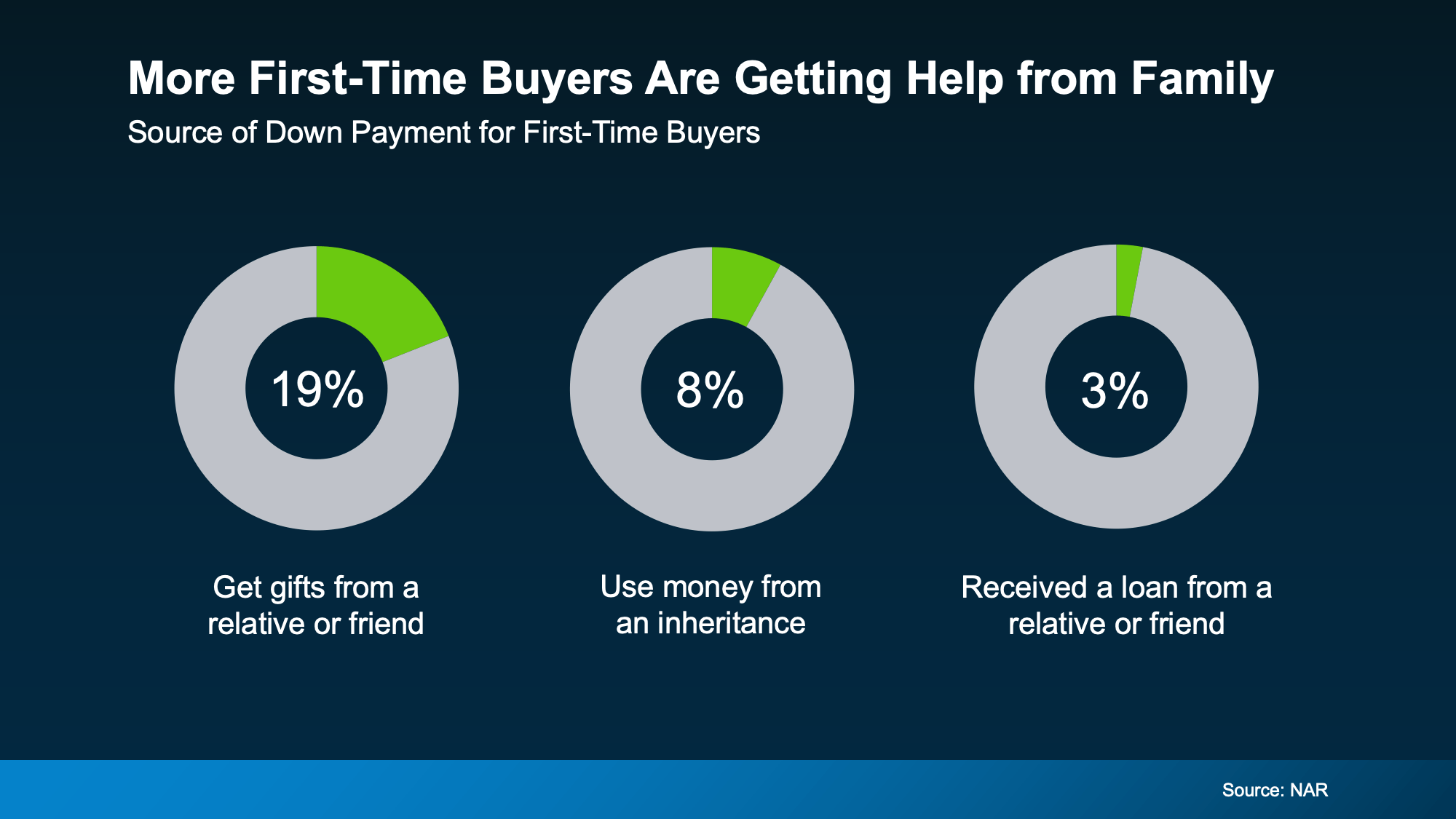

More First-Time Buyers Are Already Getting Help

If you’re wondering whether helping with a down payment is unusual—it’s not.

According to the National Association of Realtors (NAR):

- 19% of first-time buyers receive a gift from a relative or friend

- 8% use money from an inheritance

- 3% receive a loan from a relative or friend

Here’s the breakdown:

Nearly 1 in 5 first-time buyers receive gift funds.

This is already happening at scale. It’s becoming part of how families create access to homeownership in today’s market.

In The Woodlands, where demand remains strong and inventory fluctuates, having access to funds upfront often determines whether a buyer can compete confidently.

When you remove the savings delay, you move the timeline forward.

This Is About Opportunity, Not Obligation

Every family’s financial situation is different.

Helping with a down payment is not an expectation. It’s not an obligation. It’s a strategic choice.

For some, that help might look like:

- Covering 3% to 5% down

- Contributing to closing costs

- Providing bridge financing

- Assisting with earnest money

Even a relatively small amount can shift a buyer from “almost ready” to “ready now.”

And when you think about what homeownership provides—stability, equity growth, and long-term wealth building—it becomes more than a transaction. It becomes a launch point.

You experienced firsthand what owning a home did for your net worth. Helping your family access that same opportunity could compress their financial timeline by years.

What This Looks Like in The Woodlands

The Woodlands remains one of the most desirable markets in our region. Demand stays steady because of lifestyle, amenities, and overall quality of living.

For younger buyers here, the challenge is rarely desire. It’s readiness.

We often see buyers who qualify for a mortgage but need additional time to save for their down payment. When that gap is filled through family support, their options expand immediately.

They can:

- Stop renting

- Lock in a payment

- Start building equity

- Participate in appreciation

If you’re curious what your equity could realistically provide—whether that’s $25,000 or significantly more—we can run a current home valuation and discuss scenarios confidentially.

Scheduling a call allows us to:

- Estimate your equity position

- Discuss market conditions in The Woodlands

- Review lending guidelines for gift funds

- Explore timing strategies

Clarity changes decisions.

Common Questions Homeowners Ask

Will this hurt my retirement plan?

Not if it’s done thoughtfully. Many homeowners have more equity than they realize, and using a portion may still leave a strong financial cushion.

Are there tax implications?

Possibly. Gift limits and reporting requirements can apply. Always consult a CPA or financial advisor.

Do lenders allow gift funds?

Yes. Most loan programs allow gift funds, though documentation is required.

Is this becoming more common?

Absolutely. The NAR data confirms it’s already part of how first-time buyers enter the market today.

The Bigger Picture

The decision isn’t just about money.

It’s about accelerating opportunity.

Instead of waiting years for a down payment to accumulate, your equity could compress that timeline dramatically. In a market like The Woodlands, timing matters. Inventory shifts. Interest rates fluctuate. Opportunities appear and disappear.

When buyers are prepared financially, they move confidently.

That confidence often makes the difference.

Final Thoughts

If you’ve built substantial equity over the years, you may have more influence than you think over the next generation’s ability to buy a home.

The largest hurdle today isn’t rates. It isn’t price predictions. It’s upfront cash.

And that’s something you may be uniquely positioned to solve.

At The McClung Group, we help families in The Woodlands think strategically about real estate—not just for today, but for long-term legacy planning.

If you’re wondering what your home equity could make possible for you or someone you love, schedule a call. We’ll review your options clearly and privately so you can make an informed decision.

Sometimes the most meaningful investment isn’t the one you make for yourself—it’s the one that changes someone else’s future.

Schedule a Conversation

If you’re ready to explore your equity position or discuss how to help a family member buy in The Woodlands, schedule a call with The McClung Group. We’ll walk through the numbers and help you decide what makes sense for your goals.