- Categories :

- More

Market Review 2025: US Stocks Ride Rocky Road to a Third Straight Year of Gains

By:

![]() Avion Wealth

| Published 01/29/2026

Avion Wealth

| Published 01/29/2026

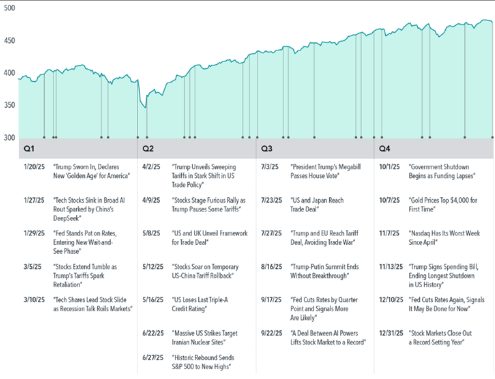

US stocks notched their third year in a row of double-digit gains, but it wasn’t the smoothest ride. The S&P 500 hit records in the winter that were followed by a spring swoon. After powering past that to new highs in the fall, the markets cooled a bit along with the temperatures. Still, the S&P 500 was up 17.9% for the year and closed near record levels. The climb came despite tariff uncertainty, interest rate changes, and concerns about the durability of AI’s gains—not to mention the longest government shutdown in US history. Global stocks rose (see Exhibit 1), with returns in developed international and emerging markets better than those in the US. In the bond market, US Treasuries were higher for the year, and the benchmark 10-year yield fell to just above 4%.1

Technology companies were below earlier highs at year’s end, but the tech-heavy Nasdaq still advanced 20.9% in 2025. Just months after reaching $4 trillion, NVIDIA became the first public company to reach a market capitalization of $5 trillion, though it wouldn’t hold that level. The headline names associated with artificial intelligence have been strong performers in recent years. But diversified equity portfolios don’t need to chase a few big names to have exposure to AI—the technology touches many types of businesses. Broad diversification can help investors avoid missing out on these winners, wherever they show up.

The US Federal Reserve cut the federal-funds rate by a quarter point three times, in September, October, and December, to a range between 3.5% to 3.75%, the lowest level in three years.2 In its December statement, the Fed cited labor-market worries as it lowered rates while also noting rising inflation and that not all members supported the rate decrease. But while investors may worry about the impact of Fed rate changes, market interest rates and the federal-funds rate don’t always move as one—the 10-year Treasury yield, for example, hasn’t always gone in the same direction as the fed-funds rate.

In a departure from recent years, developed international stocks fared better than their US counterparts. The MSCI World ex USA Index gained 31.9%, outpacing the S&P 500 by the widest margin since 1993 and serving as a reminder of the potential benefits of an internationally diversified portfolio. Emerging markets fared even better than developed markets, with the MSCI Emerging Markets Index rising 33.6%. Global equities, as measured by the MSCI All Country World Index, rose 22.3% for the year.

Likewise, investors who targeted value stocks outside the US were rewarded; however, value lagged growth in the US. Large caps outperformed small caps in the US and globally, but international small value was among the best-performing asset classes of the year. Longer term, US small value has been one of the best-performing asset classes since 2000. That has included a period of strong performance for the large cap S&P 500: Over the past 10 years, it returned 14.8% annually. That’s a notable deviation from large caps’ long-term average, whereas the returns of small caps have been more in line with their historical performance over that same period. Elsewhere, high profitability stocks were outpaced by low profitability stocks in global developed markets in 2025, while the opposite was true in emerging markets.

In the bond market, US Treasuries returned 6.3%, sending the yield on the benchmark 10-year Treasury down to 4.18%. The broader bond market also posted gains during the year, with the Bloomberg US Aggregate Bond Index up 7.3%, its best annual return since 2020. The Bloomberg Global Aggregate Bond Index (hedged to USD)—a broad benchmark of sovereign and corporate debt—rose 4.9% for the year.

Investors showed increased appetite for gold in 2025, pushing prices up more than 50% to above $4,000 per ounce for the first time.3 Some market participants view gold as a hedge during economic downturns or against inflation. But since 1970, gold has often experienced large price swings relative to annual inflation. Over the same period, gold prices showed little relation to fluctuations in the US GDP. Whether gold was up or down doesn’t appear connected to what was happening in the economy. Since markets tend to reflect expectations for the economy in advance, it’s not clear holding gold provides additional protection against adverse economic developments.

A better way to cope with market volatility may be to simply pay less attention. Just this past year, if you had gone to sleep on April Fools’ Day and checked your investment portfolio a month later, you might have assumed the market had been relatively calm. But for investors who spent the month tracking daily returns, the experience likely felt more disruptive. April 2025 turned out to be one of the most volatile months in recent history, as market participants were processing new information about tariffs and trying to make sense of what the developments might mean for businesses, investors, and the global economy.

The same thinking can guide investors’ approach over longer time periods—especially when looking at data across many years or even decades. With reliable stock data stretching back to 1926, we are, as of this year, now able to consider a full century of stock returns. Doing so gives further credence to the merits of focusing on the long run. A short-term view of yearly gains and losses shows what may appear as wild swings in the market, but a long-term view reveals a fairly steady growth of wealth over the 100-year period.

To your success,

The Avion Wealth Team

Footnotes

Returns are based on the Bloomberg US Treasury Bond Index as of December 31. Bloomberg data is provided by Bloomberg Finance LP. Source for US Treasuries: US Department of the Treasury.

The federal-funds rate is the overnight interest rate at which one depository institution (like a bank) lends to another institution some of its funds that are held at the Federal Reserve. Source: “Federal Reserve Issues FOMC Statement,” US Federal Reserve, December 10, 2025.

Spencer Kimball, “Gold Price Reaches $4,000 an Ounce for the First Time Ever,” CNBC, October 7, 2025.

")

")